All eyes will be on Federal Reserve’s annual Jackson Hole symposium’s speech by Fed’s Chairman Powell on Friday, with investors hoping for indications on when the Fed will begin tapering the monetary stimulus that has powered stocks to record highs since the COVID-19 pandemic.

The economic calendar also features a string of economic data, including US personal spending and durable goods orders. Earnings will continue with Best Buy ($BBY) , Dell ($DELL) and HP ($HPQ) among the companies reporting.

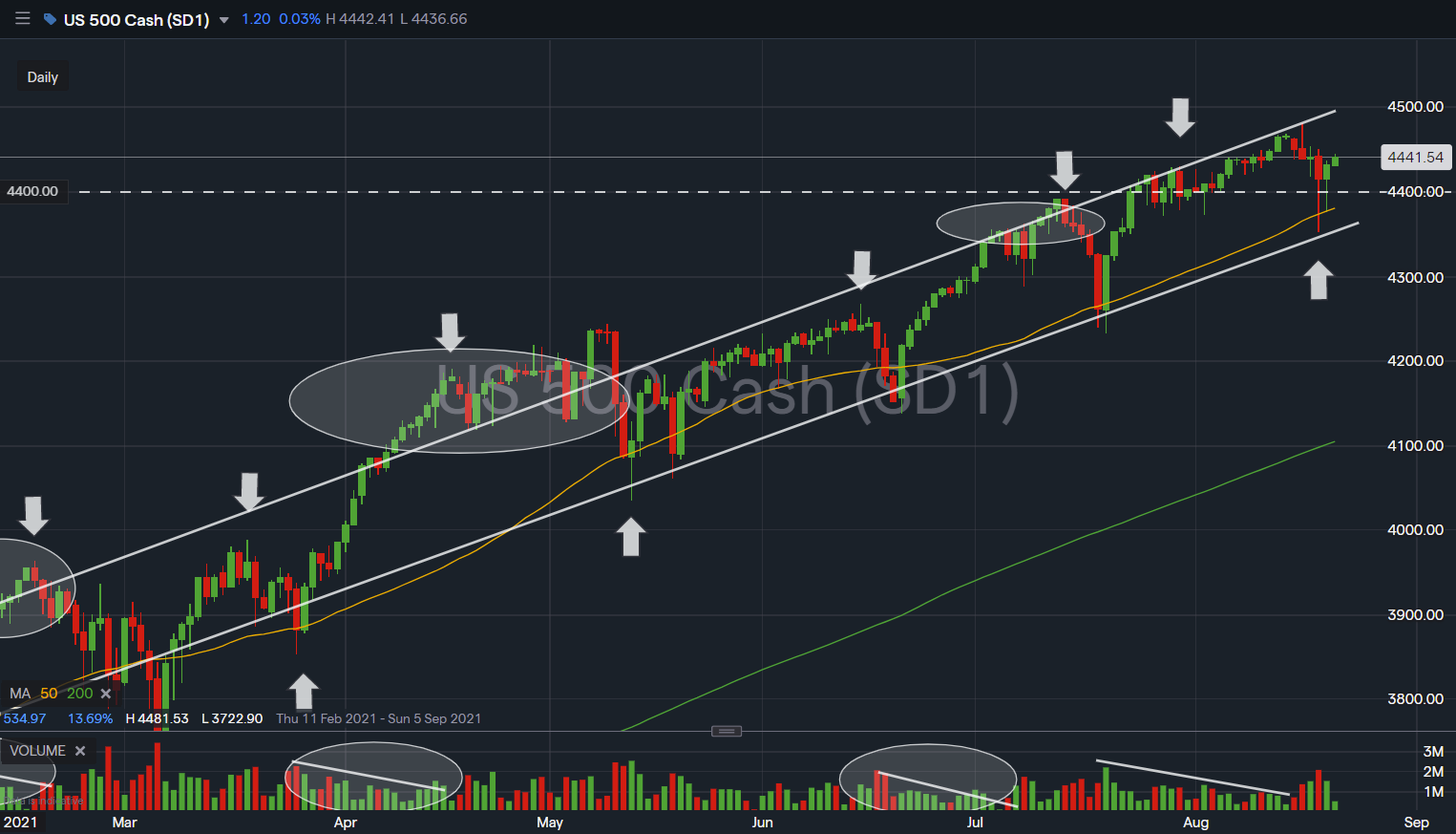

While stocks are still hovering near record highs all three major U.S. indexes posted weekly losses last week after tumultuous trading and more volatility looks likely to be in store in the week ahead.

Here’s what you need to know to start your week.

$SPX have successfully corrected out a 3 weeks price-volume divergence, supported at the 4,400 level that was highlighted in the previous week.

With more volatility looks likely to be in store in the week ahead, the immediate support to watch for $SPX this week remains at 4,400 level; a further retest of immediate support along with a break of its 20D Moving Average.

Jackson Hole

The Fed is expected to communicate its plans for slowing its $120 billion per month asset purchase program, the first step down the road to eventual interest rate hikes.

But the prospect of stimulus being reduced at a time when the rise of the highly contagious delta variant is clouding the outlook for the economic recovery has spooked markets.

The Fed announced Friday that its annual symposium would be held online instead of at its usual location in Jackson Hole, Wyoming. The symposium will run from Thursday through Saturday, but the main event will be the keynote speech by Fed Chair Jerome Powell.

Last week’s minutes of the Fed’s July meeting pointed to a greater likelihood of a taper beginning this year and Powell’s speech could be the last hint at the central bank’s next steps before its September policy meeting.

Economic data

Besides the Fed’s annual get-together market watchers will also have to digest a slew of economic data in the week ahead, including reports on home sales, durable goods and personal income and spending.

Figures on existing home sales are released on Monday, followed a day later by a report on new home sales. Data on durable goods orders is due out on Wednesday and initial jobless claims numbers will be released Thursday. Revised figures on second-quarter GDP are also out on Thursday but are expected to show little change.

Friday brings the release of personal spending data along with the core PCE price index, the Fed’s preferred gauge of inflation, which has been running near a 30-year high.

Earnings

While the second-quarter reporting season has essentially run its course, there are still some companies left to report during the week.

JD.com ($JD), Palo Alto Networks ($PANW) and Madison Square Garden ($MSGS) are reporting on Monday. Best Buy ($:BBY), Nordstrom ($JWN), Urban Outfitters ($URBN) and Toll Brothers ($TOL) are some of the names reporting on Tuesday. Salesforce ($CRM) and Dick’s Sporting Goods ($DKS) are due to report on Wednesday. HP, ($HPQ) Dell ($DELL), Gap ($GPS), Abercrombie and Fitch ($ANF), Dollar General ($DG), Dollar Tree ($DLTR), Ulta Beauty ($ULTA) and Peloton ($PTON) will all report on Thursday.

It’s been a stellar earnings season – so far 476 of the companies in the S&P 500 have posted results and of those, 87.4% have beaten consensus.