This week is a holiday-shortened week as US Markets will be closed on Monday in observance of US Labor Day.

As Investors are weighing the impact of last Friday’s surprisingly soft August jobs report, Stocks are likely to look beyond the numbers and latch onto the latest data on labor and inflation in the coming week’s jobless claims and producer price index (PPI). Comments by Federal Reserve officials will also be in focus after the disappointing August employment report.

Stock markets are likely to remain supported after the jobs data undermined the argument for near-term tapering. Meanwhile, all eyes will be turning to the European Central Bank’s debate over whether it should start reducing its massive PEPP asset purchase program amid brighter prospects for the bloc’s economic outlook.

China is also set to release data on trade and inflation which is expected to underline that the recovery in the world’s number two economy is losing momentum.

Here’s what you need to know to start your week.

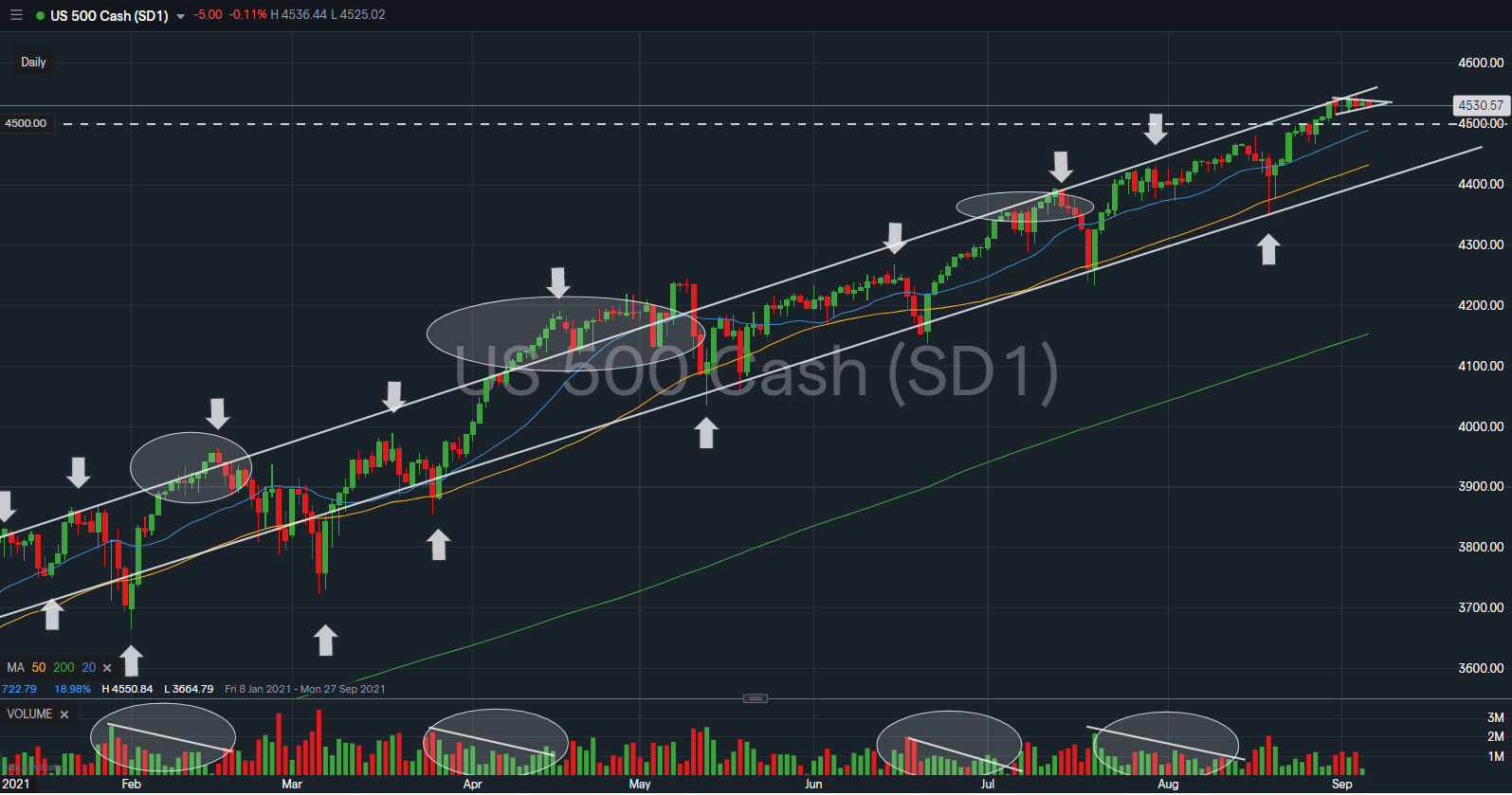

$SPX medium term trend channel remains intact, with no violation of its upper and lower bound trendline since the Bullish Reversal supported by its 50DMA highlighted in the previous week. $SPX remains trading neatly above its 20DMA over the past 14 consecutive trading session. At the current junction, $SPX is consolidating within a bullish pennant pattern, signifying trading activity could remain subdued as traders return after the long weekend.

The immediate support to watch for $SPX this week is revised upward towards 4,500 level; a break down of its current consolidated pennant pattern.

U.S. data

Friday’s PPI data for August will show how inflation pressures are shaping up after July data showed the largest annual increase in over a decade, as the swift economic recovery caused a mismatch between supply and demand.

While the Fed has indicated that higher prices will likely prove transitory some worry that persistent price pressures could prompt the Fed to roll back easy money faster than expected.

Weekly jobless claims data Thursday will also be closely watched after the Labor Department reported Friday that the economy added just 235,000 jobs in August, falling far short of economists’ estimate of 750,000.

Hiring in the leisure and hospitality sector stalled amid a resurgence in COVID-19 infections. But the unemployment rate fell to 5.2% from 5.4% in July and July job growth was revised sharply higher, pointing to underlying strength in the economy.

Fed speakers

Market participants will be watching out for any fresh clues on tapering from Fed officials in the wake of Friday’s disappointing jobs report.

The labor market remains the key touchstone for the Fed, with Chair Jerome Powell indicating last week that reaching full employment was a pre-requisite for the central bank to start paring back its asset purchases.

New York Fed President John Williams, who is viewed as close to Powell, is to speak about the economic outlook at an event on Wednesday.

Gamestop $GME

Investors will be watching out for quarterly results from video game retailer GameStop ($GME), whose wild ride this year put a spotlight on retail investors’ mania for so-called meme stocks that some say is one sign of irrational exuberance in markets.

ECB meeting

The ECB meets on Thursday against a background of calls from several hawkish policymakers to begin slowing its pandemic-era asset purchase stimulus program given a recent spike in inflation.

Inflation in the euro area has surged to a 10-year high of 3%. The ECB has indicated that any increase in inflation is likely to be temporary, but some hawkish officials have recently diverged from this view.

Markets are starting to react to the potential for more sustained euro zone inflation and reduced stimulus from the ECB.

China data

On Monday China releases August trade data which will be followed on Wednesday by figures on both consumer and producer inflation, also for last month.

The reports come after a recent run of weak economic data which showed that the recovery in the world’s second largest economy is running out of steam amid restrictions to curb the spread of the Delta variant.

Activity in China’s services sector slumped into sharp contraction in August, a private survey showed on Friday and a similar survey of the manufacturing sector showed that factory activity contracted for the first time in almost one-and-a-half years last month.

The slowdown has fueled expectations Beijing will roll out more support measures to revitalize growth.