It is a relatively busy week ahead in the US on the economic data front. This Tuesday’s U.S. inflation numbers could help dictate market direction in the coming week amid concerns that persistent rising inflation could prompt the Fed to roll back emergency stimulus measures. The timing of when central banks choose to scale back economic stimulus has been a key driver of market sentiment amid concerns over rising inflation.

Elsewhere on economic data, US retail sales and industrial production numbers for August are seen pointing to a decline in domestic trade and modest factory activity growth. Numbers will be out on Thursday.

The UK is also due to release what will be closely watched inflation data, along with updates on employment and retail sales. Appearances by European Central Bank officials may shed more light on last week’s decision to scale back bond purchases. Meanwhile, data from China is likely to underline that the pace of the recovery in the world’s number two economy is slowing.

Here’s what you need to know to start your week.

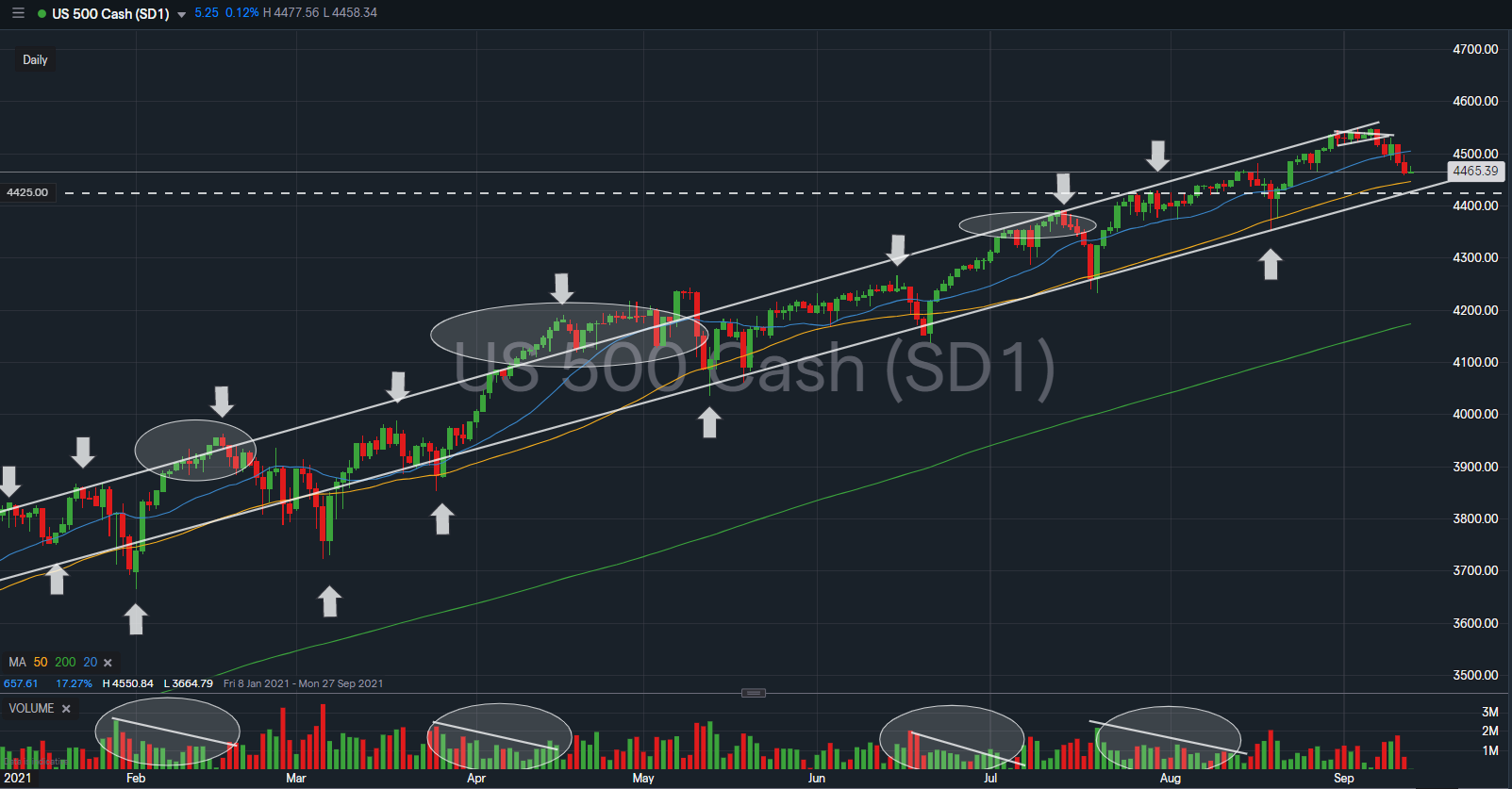

$SPX medium term trend channel remains intact, with no violation of its upper and lower bound trendline since the Bullish Reversal supported by its 50DMA highlighted in the earlier weeks. $SPX is now trading below its 20DMA after the failure of its Bullish Pennant consolidation, spiraling down towards its 50DMA that has pivoted the index since November 2020.

The immediate support to watch for $SPX this week is at 4,425 level; a break down of 50DMA along with its short term support level.

U.S. inflation

Tuesday’s data on consumer price inflation will be the highlight of the economic calendar amid an ongoing debate over whether the current spike in inflation is likely to fade as the imbalance between supply and demand causing price increases in recent months eventually eases.

In July, price increases slowed but remained at a 13-year high on a yearly basis amid tentative signs inflation has peaked.

Market watchers will also be looking at Thursday’s figures on retail sales, which are expected to decline for a second straight month.

UK data

Last week Bank of England governor Andrew Bailey warned that the economic rebound in the UK is slowing, so this week’s data on inflation, employment and retail sales will be closely watched, particularly ahead of the Bank of England’s upcoming policy meeting on Sept 23.

July data showed that inflation slowed to 2%, while retail sales fell 2.5% month-on-month.

Tuesday’s jobs data will also be in focus amid labor shortages and a record 8.8% increase in wage growth in June. The end of furlough schemes may push people into the jobs market, but skills shortages risk fueling price pressures driven by supply bottlenecks and commodity prices.

ECB speakers

In the euro zone, ECB Chief Economist Philip Lane and Bank of Finland Governor Olli Rehn are both due to make appearances, with investors hoping for more insights into last week’s decision to pare back emergency bond purchases over the coming quarter.

The move is a small first step towards unwinding the emergency stimulus the ECB deployed to bolster the euro zone economy during the coronavirus pandemic.

ECB President Christine Lagarde was eager to stress that the move wasn’t the start of tapering.

The move by the ECB to trim bond purchases is expected to be followed by the Fed later this year, despite the disappointing August U.S. jobs report.

China data

China is to release data on industrial production, retail sales and fixed asset investment on Wednesday, which will show the economic impact of a widespread Covid outbreak in August, which saw Beijing partially close the world’s third-busiest container port and impose fresh restrictions across some areas of the country.

While the latest outbreaks have been largely contained the Chinese economy is still facing headwinds.

While exports have remained strong, boosted by robust global demand domestic demand has faltered amid virus containment measures, supply bottlenecks, tighter measures to tame property prices and a campaign to reduce carbon emissions.