Investors will be waiting for the FOMC minutes due Wednesday for further clarification on the next monetary policy steps to direct the market in the week ahead. At its July meeting, the Federal Reserve left monetary policy unchanged, but said asset purchases could start being reduced soon amid signs of a solid recovery in the US labor market and temporary inflationary pressure, and despite the lingering threat of the Delta variant.

On the economic data front, latest U.S. retail sales data, along with a flurry of retail earnings will also keep the focus on consumer strength. Several large retailers including Walmart ($WMT), Target ($TGT), Macy’s ($M), Lowe’s ($LOW) and Home Depot ($HD) will be reporting quarterly results.

Chinese data will give a snapshot of how the economy is faring as the delta variant of the coronavirus bears down and New Zealand looks set to be one of the first of the world’s advanced economies to raise interest rates in the pandemic era.

Here’s what you need to know to start your week.

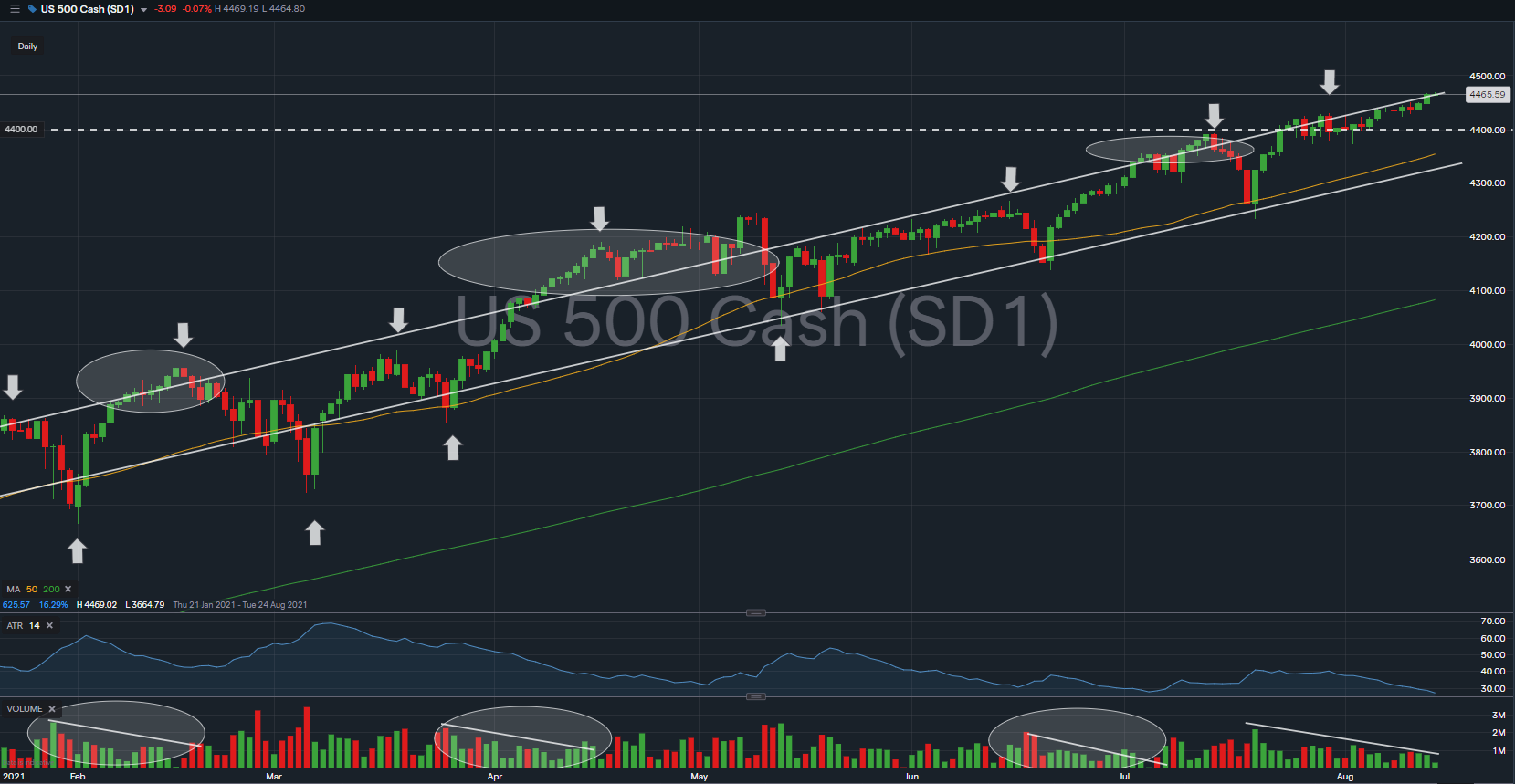

$SPX remains above its multi-month long trend channel that was earlier highlighted. Every break out of $SPX trend channel resistance has been met with a rejection (6 times since 2021). It is also important to note of the diminishing volume observed, reflecting a short term price-volume divergence in this run up.

The immediate support to watch for $SPX this week is revised up to 4,400 level; a retracement towards its minor resistance-turned-support, and its current 20DMA level.

Federal Reserve minutes

On coming Wednesday the Fed will release the minutes of its July meeting, which will be scrutinized for policymakers’ views on when to start scaling back the Fed’s monthly bond purchases, as well as their outlook on the economy.

Last month Fed officials declared the recovery intact despite the rise of the delta variant and since then the stronger-than-forecast July jobs report prompted several policymakers to suggest the tapering of asset purchases might start sooner rather than later.

U.S. retail sales

The U.S. economy is growing strongly but the spread of the delta variant remains a headwind so upcoming economic data will provide a fresh insight into consumer demand after a report on Friday showing that consumer confidence fell to its lowest level in a decade. Consumer spending accounts for around 70% of U.S. economic output.

Investors will be eyeing Tuesday’s U.S. retail sales data to see whether the shift in spending from goods to travel, leisure and services, which aren’t reflected in retail sales, continued in July.

Economists are forecasting a 0.2% fall, amid another expected steep decline in auto sales.

Other reports on the slate include industrial production on Tuesday and initial jobless claims Thursday as well as the Fed’s Empire State manufacturing index on Monday and the Philadelphia Fed manufacturing survey on Thursday.

China recovery

China, which is dealing with its largest outbreak of Covid since the early days of the pandemic, has imposed mass testing and travel restrictions, crimping economic activity.

Several Wall Street investment banks, including Goldman Sachs last week cut their China growth forecasts for the rest of the year.

Data on retail sales, industrial production and fixed asset investment all due out on Monday will show how the economy fared in July. The numbers are expected to slow, adding to concerns that the recovery in the world’s second-largest economy is losing momentum.

The recovery from the pandemic has been uneven in China, with export demand driving most economic growth, while domestic demand has returned more slowly.

New Zealand rate hike

The Reserve Bank of New Zealand bank meets on Wednesday and looks set to become the first major economy to raise interest rates since the pandemic hit as its red-hot economic recovery continues.

Super-strong jobs data have cemented expectations of a hike, which would be New Zealand’s first since mid-2014. This is in sharp contrast to 2020, when rates were slashed 75 basis points to 0.25% and a move below zero became a real possibility.