Focus this week for investors will be on the minutes from the last Federal Reserve’s last policy meeting that are due on Wednesday. There will be hopes that they might provide some clarity on policymakers’ next moves. Last month, the Federal Reserve left monetary policy unchanged, despite acknowledging a “temporary” rise in inflation and an improvement in the economic outlook.

Additionally, with a strong U.S. Q1 reporting season winds up; retailers are getting started – Walmart ($WMT), Target ($TGT), Home Depot ($HD), Lowe’s ($LOW), L Brands ($LB) and Ralph Lauren ($RL) release results this week. The numbers will show how consumer spending is shaping up as the economy rebounds from the coronavirus. And after U.S. consumer prices rose by the most in nearly 12 years in April, investors will want to see whether price pressures are building for companies. Also, the CDC said fully vaccinated people can stop wearing face masks and end physical distancing in most settings.

Here is what you need to know to start your week.

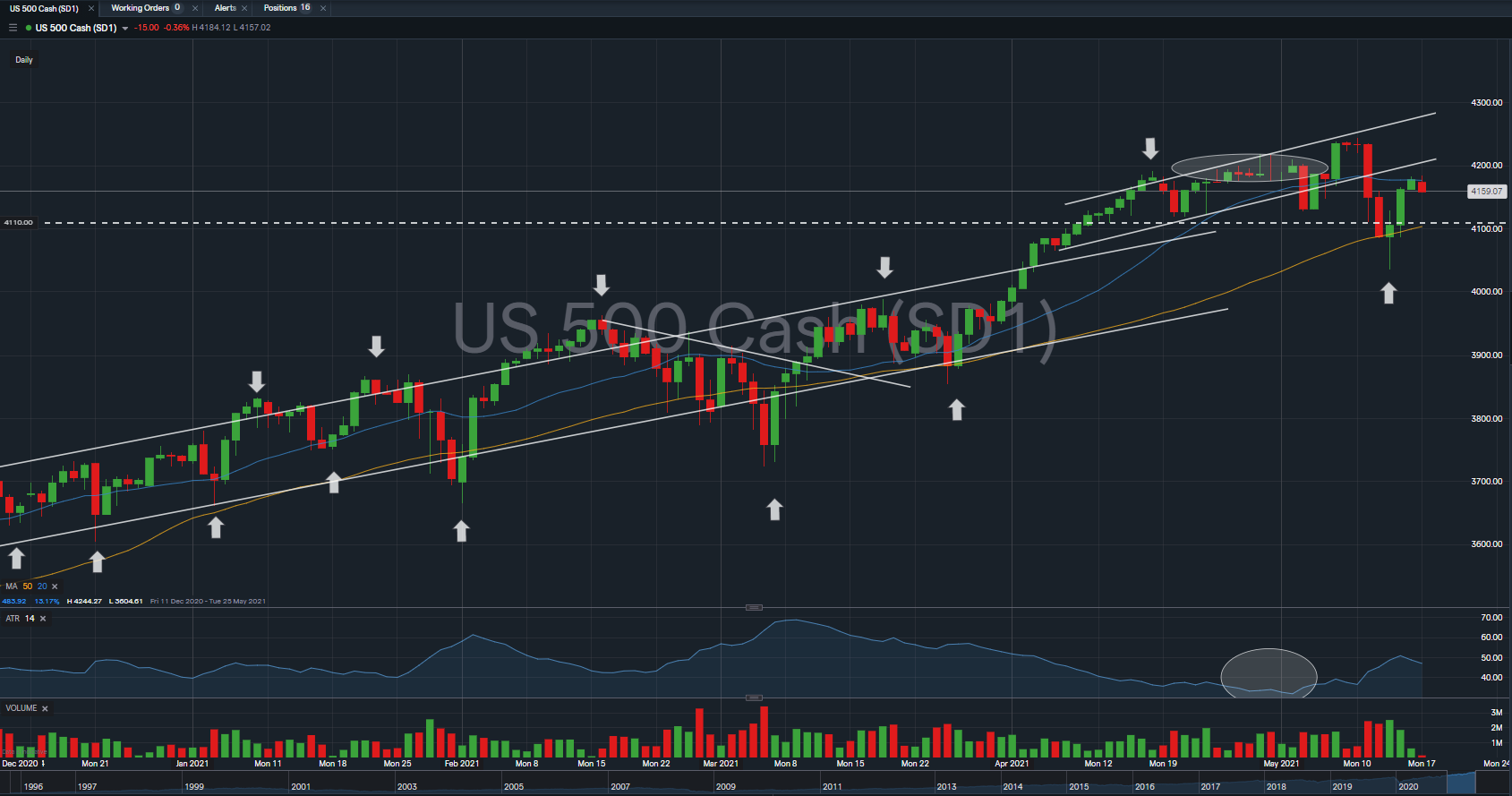

The benchmark index ($SPX) erased all gains for the month of May, losing -1.31% (-55.4 points), with trading floors awashed with red after a higher-than-expected reading on US inflation fuelled bets of potential tapering of the Federal Reserve’s bond-buying before year’s end.

$SPX is currently trading below its 20DMA, along with an failure attempt to break its minor classical support level of 4,110 highlighted last week. It is also worth to note that $SPX ATR-14 have rebounded from its year low level of 40 points/day, with a 20% increment towards 50 points/day during the week. Trading volume resumption back to its normalcy is also witnessed on 13th May, the day of the rebound.

The immediate support to watch for $SPX remains at 4,110 level, a minor support turned major support level, coinciding with its 50DMA.