US markets will be closed on Thursday and will close early on Friday for the Thanksgiving holiday.

The market will be paying close attention to Wednesday’s FOMC meeting minutes for fresh insights into the impact of soaring inflation on the future path of interest rates. Markets may also reprice the timing of future rate hikes if President Joe Biden were to promote current Fed Governor Lael Brainard to the Fed Chairman position, while the prospects of lower interest rates for longer could see a sell-off in U.S. Treasuries prompted by expectations for higher inflation.

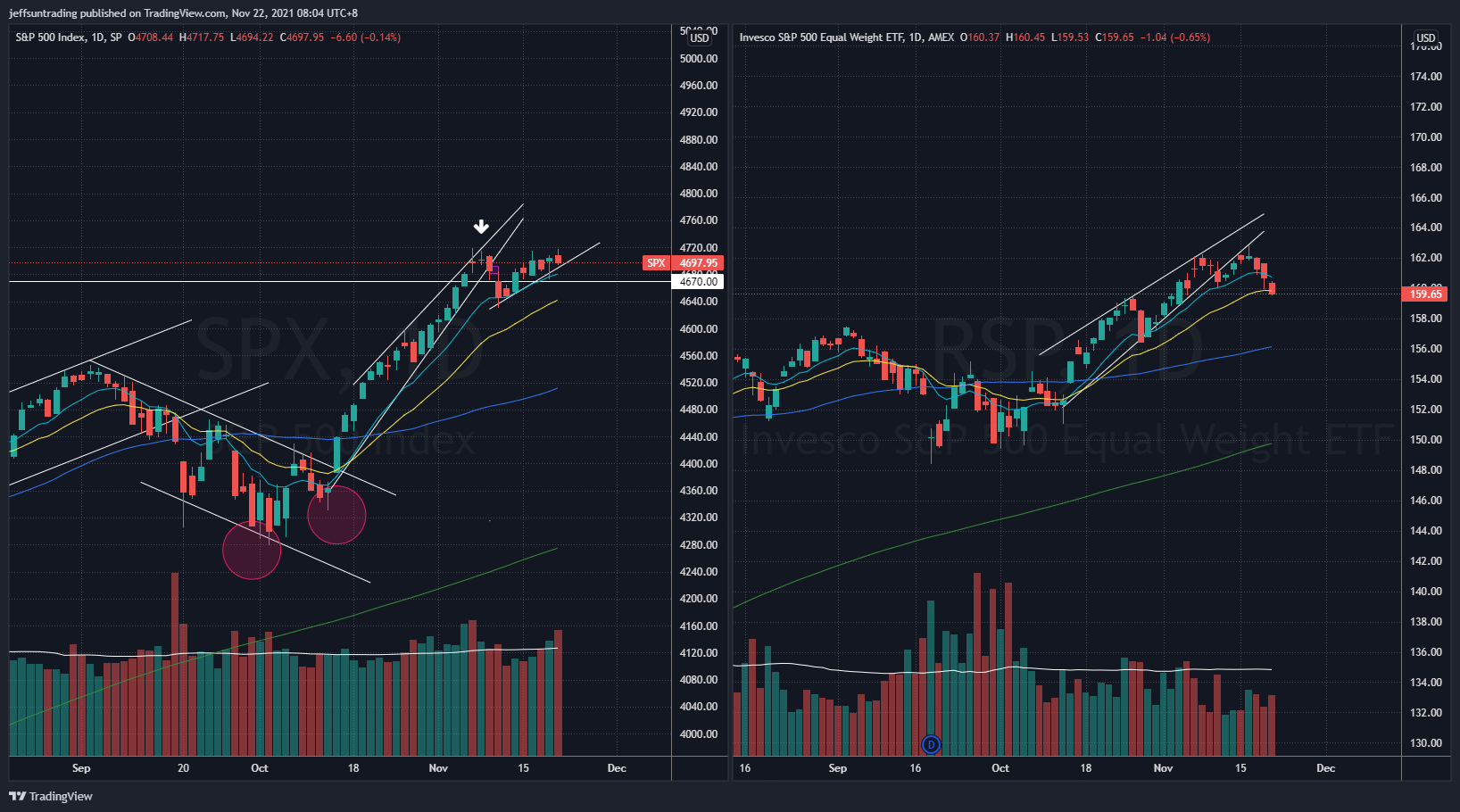

With $SPX (S&P 500) gaining +0.32% for the week, the bearish Rising Wedge formation of $RSP (S&P 500 equal weight) played out with a -1.24% loss. The correction in $RSP have reflected signs of fatigue in this market rally. Similar behavior of divergence is also witnessed between $QQQ and $QQQE.

Last week’s leading sectors:

$XLY (Consumer Discretionary) +3.76%

$XLK (Technology) +2.39%

$XLU (Utilities) +0.98%

$SPX +0.32%

This week’s watchlist:

$ABNB, $AMAT, $AVTR, $ZIP, $BBW, $KLIC and 42 more names.

There will also be a flurry of U.S. economic data on Wednesday ahead of the holiday, while PMI data out of the euro zone, UK and the U.S. during the week will outline the impact of supply chain issues and inflation on business activity.

Here’s what you need to know to start your week.

Market Technicals

$SPX (S&P 500) vs $RSP (S&P 500 Equal Weight)

The immediate support to watch for $SPX this week is at 4,670 level, a break of its short term uptrend line and 10DMA.

Fed minutes

On Wednesday, the Fed will publish the minutes of its November meeting, in which policymakers decided the U.S. economy was strong enough to start scaling back its pandemic-era asset purchase program, put in place to bolster the recovery.

Since then, the economic recovery has continued to accelerate, with job gains picking up and inflation continuing to soar, leading Fed Vice Chair Richard Clarida to call last week for a discussion on a quicker taper to position the Fed to hike rates sooner.

Last Thursday, Chicago Fed President Charles Evans, known as a policy dove, said he is “more open-minded” to raising interest rates next year than he was six months ago. Separately, Atlanta Federal Reserve President Raphael Bostic has signaled his support for a mid-2022 rate hike.

The Fed is due to publish fresh quarterly forecasts following its next meeting in mid-December and these may give a better read on how much policymakers’ views have altered.

Biden’s Fed pick

The White House said last week that President Joe Biden will likely decide before Thanksgiving whether to keep incumbent Fed Chair Jerome Powell in place for another term or promote current Fed Governor Lael Brainard to the position.

Analysts expect some stock market volatility around the announcement, particularly if Brainard is chosen.

Powell, whose term is due to end in February next year, was appointed in 2018 by then-President Donald Trump. Brainard, who has been on the Fed board since 2014 is favored by progressive Democrats and is seen as more dovish than Powell.

If Brainard is appointed markets may reprice the timing of future rate hikes, while the prospects of lower interest rates for longer could see a sell-off in U.S. Treasuries prompted by expectations for higher inflation.

U.S. data dump

The U.S. is to release a string of economic data on Wednesday before markets close for Thursday’s holiday. The highlight will be figures on personal income and spending, which includes the core PCE price index, rumored to be the Fed’s favored inflation gauge.

The economic calendar also features a revised data on third-quarter GDP, initial jobless claims, durable goods orders, new home sales and consumer sentiment.

Reports on existing home sales and November PMI data, which is expected to show only a modest improvement will be released on Monday and Tuesday, respectively.

PMIs

While November PMI data out of the U.S. is expected to show a modest uptick in business activity, similar surveys from the euro zone and the UK are expected to show activity in the manufacturing and services sectors is slowing.

Rising infection numbers are leading to renewed restrictions in some parts of Europe, while spiking gas prices are fueling inflation, compounded by a global supply chain crunch.

The European Central Bank is coming under increasing pressure to tighten its ultra-loose monetary policy to offset the hit to households spending power, but ECB President Christine Lagarde has pushed back, arguing that tightening policy now could choke off the economic recovery.

Meanwhile, the Bank of England looks set to become the first of the world’s big central banks to raise rates since the onset of the pandemic, with investors and economists expecting a rate hike at its upcoming December 16 meeting.